The Weekly Compass 27/04/26

John Mullane

John Mullane

27.04.2026

The Weekly Compass: 27/4/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: A pivotal week for markets with 5 of Mag-7 reporting.

The Week That Was

Global equity markets moved 0.5% higher in euro terms last week, in what was a mixed week for markets, reflecting a combination of solid earnings alongside continued uncertainty around a resolution to the US/Iran conflict. The S&P 500 reflected this two-way tussle, with the Energy and Technology sectors by far the strongest performers, as the index climbed 0.6% in local currency terms.

European equities were more challenged on the week, ending down 2.3%, reflecting concerns on the growth outlook, particularly in Germany, which weighed particularly heavily on the Banking and Travel sectors. Oil prices rebounded sharply, with Brent up 16.5% following three weeks of losses, which in turn pushed global commodity prices 4.3% higher on the week. Global bonds were largely unchanged on the week in euro terms; however, expectations that the Department of Justice (DOJ) would drop its probe into Fed Chair Powell did see the US 10-year retrace to 4.30% on Friday.

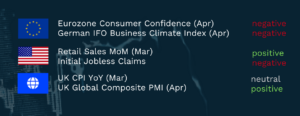

Summary Economic Releases

The Week Ahead

Asian markets moved higher this morning, buoyed by a rally in the tech sector along with reports that Iran submitted an offer to the US which would extend the ceasefire and open the Strait of Hormuz. This will clearly ease concerns that the peace talks had stalled; however, given the proposal involves postponing nuclear negotiations, it is uncertain if it will be accepted by the US. While Brent crude has eased from its recent highs, prices remain elevated at around $107 per barrel. Although a resolution appears increasingly likely, with equity markets rebounding to fresh all-time highs, we believe the near-term risk-reward balance warrants a more cautious positioning by investors.

Corporate earnings season continues at pace in the week ahead, with one-third of the S&P 500 due to report. Results from five of the Mag-7, namely Microsoft, Alphabet, Amazon, Meta and Apple, will be among the highlights. Investor attention will centre on cloud demand trends, advertising momentum, and the scale and returns of ongoing investment in AI infrastructure. Many names of Irish interest will also have earnings releases, including CRH, AIB, Bank of Ireland, Smurfit Westrock and Glanbia, where the focus will be on organic growth drivers and overall margin strength, as whey input costs need to be managed. For the banks, growth in deposits and loans will be closely watched, with net interest margins also a focus, and for CRH and Smurfit, energy input costs and pass-through outlook will be important factors.

From an economic perspective, on Tuesday a slight deterioration in the confidence of US consumers is expected for April, on the back of higher petrol prices. On Wednesday, Kevin Warsh’s nomination moves to the Senate Banking Committee, whilst Jerome Powell is set to give his final address as Fed Chair. No change to rates is expected given the step-up in inflation, which should be on show on Thursday with the release of March’s core PCE of 3.2% YoY. Thursday should also see the BoE and ECB look through recent spikes in CPI and leave rates on hold; however, persistent inflation could open the door to a hike as early as June for the latter. Following a government shutdown-induced slowdown in the last quarter of 2025, US GDP is expected to rebound sharply to 2.2% YoY when released on Thursday, buoyed by tech-related business investment. In contrast, Eurozone GDP is set to slow to 0.9% YoY in Q1 26, reflecting impacts of the war in Iran.

Opportunities this week:

• CRH – (Overweight, PT $142, c. 20% upside) – Look ahead to Q1 results and Holcim read-across

• Smurfit Westrock (Overweight, PT $55.60, +39% upside) – Look ahead to Q1 results, PT change and Mondi read-across

• Kingspan (PT €94.60, +19% upside) – Readthrough post peer results last week

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland