The Weekly Compass 20/04/26

John Mullane

John Mullane

20.04.2026

The Weekly Compass: 20/4/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: Earnings season kicks into full gear in the week ahead as uncertainty on the Iran conflict lingers.

The Week That Was

Global equities moved 3.9% higher in euro terms last week, with growing evidence of easing tensions between the US and Israel and Iran and Lebanon. The S&P 500 climbed 3.6% in euro terms, led higher by a better‑than‑expected earnings season thus far and a strong rebound in the tech sector, in particular software stocks. European equities ended the week almost 2% higher, with tech again leading alongside financials. The euro strengthened modestly relative to the dollar, settling just below 1.18, however it remains below its year-to-date (YTD) highs. Oil prices declined over 5%, marking their third consecutive weekly fall and pushing global commodities down almost 2% overall. Global bonds moved marginally higher over the week on receding fears of a sustained uptick in inflation.

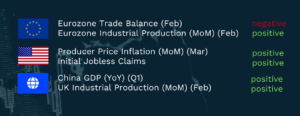

Summary Economic Releases

The Week Ahead

Asian markets moved higher this morning, led by tech‑heavy markets such as South Korea, as investors refocused on the potential of AI and bet that peak uncertainty has passed in the Middle East conflict. This is despite tensions escalating between Iran and the US over the weekend, resulting in oil prices trending over 5% higher, while the USD also rebounded following three weeks of weakness. Negotiations are slated to continue on Tuesday between both sides and whilst a resolution is likely, with equity markets back at fresh all‑time highs following a strong rally last week, greater caution is warranted.

Corporate earnings season kicks into gear with over 90 of the S&P 500 due to report in the week ahead. Key names in focus include GE, Intel, Boston Scientific and particularly Tesla. The latter will be the first of the Mag‑7 to report and is currently engaged in a strategic pivot away from auto manufacturing towards robotics. As a result, focus will be on progress at its Terafab AI compute facility, alongside commentary on robotaxi rollout and timelines. In Europe, several key market bellwethers are due to report in the week ahead, including Rio Tinto, Nestlé and in particular L’Oréal, where the market is pricing in organic sales growth of 3.75%, driven by Professional Products sales and solid growth in North America and Europe, whilst Asia is expected to remain challenged. Rio is expected to show strong iron ore production growth year-on-year (YoY) in Q1.

From an economic perspective, Tuesday’s US retail sales for March are expected to highlight evidence of strain on consumer budgets due to rising gas prices. This strain should also be evident in Eurozone consumer confidence data for April, which is expected to decline to levels not seen since the first quarter of 2023 on Wednesday. Investors will also look for clues on the potential sequencing of rate decisions when Kevin Warsh testifies at his Senate confirmation hearing. Thursday should indicate that industrial activity in the Eurozone weakened in April, linked to the conflict in Iran, with manufacturing experiencing its first month of decline in four. US initial jobless claims are also expected to tick up but remain consistent with a no‑hire, no‑fire environment. Finally, the German IFO, a reliable early gauge of business activity, is set to point to a reversal of most of the gains made since the start of the year.

Opportunities this week:

• Flutter (Overweight, PT $199, c. 82% upside) model estimate revisions and PT change

• Ryanair (Overweight, PT €30.50, c. 18% upside) recap on key strengths, strategy and investment thesis

• Supermarket Income REIT (Overweight, PT 90p, +12.2% upside) read‑through from Tesco’s solid FY26 results

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland