The Weekly Compass 16/2/26

John Mullane

John Mullane

16.02.2026

The Weekly Compass: 16/2/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: Irish corporate earnings and legality of Trump tariffs in focus this week.

The week that was

Despite strength in emerging markets and resilience in Europe, weakness in the US saw global equities trend modestly lower last week. The S&P 500 fell 1.4% on a continued rotation out of mega cap tech related names while the equal weighted index was broadly flat. European equities ended the week little changed with Healthcare and Utilities among the standout performers. Global bonds rallied by 0.9% as softer inflation data in the US saw markets price in up to 2.5 rate cuts by the Fed before year end. Global commodities moved modestly lower as demand for oil and industrial metals such as copper weakened. The Munich Security Conference also continued over the weekend where US Secretary of State Marco Rubio warned Europe that the old world order is gone and thus reemphasising the importance for Europe to boost defence spending.

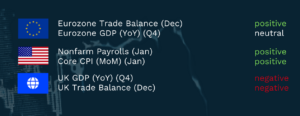

Summary economic releases

The week ahead

Asian benchmarks start the week hovering near all time highs however equities in Tokyo have trended lower on weak Japanese GDP data for Q4 2025 released on Sunday. Chinese markets are closed this week for Lunar New Year holidays where there will be hopes that 62.5bn yuan in trade in subsidies can drive a pick up in consumer spending. Profit taking saw gold drift almost 1% lower and below 5,000 dollars this morning while oil prices were broadly flat.

Corporate earnings will be a primary driver of market sentiment in what is a holiday shortened week in the US where Walmart, John Deere, Analog Devices and CRH will be among the most notable releases. For the latter, focus will be on the recent uptick in margins and the growth outlook for 2026 which is expected to continue to be driven by the US Material segment with international revenue growth also improving to 3.6% organic. Overall, 74% of the S&P 500 companies have now reported, with earnings beat rate running at over 70%.

In Europe, earnings season is close to the midway point with corporates reporting a beat rate of over 20%. This will be a particularly busy week with Nestlé and Rio Tinto due to report alongside a raft of Irish corporates including Kingspan, Kerry and IRES REIT. For the latter, investors will be focused on continued net rental income margin strength alongside a solid execution of the group’s asset recycling programme as well as commentary around proposed new rental legislation expected to be introduced on March 1st.

It will be a busy week on the macro front in the week ahead with plenty of market moving data points. On Tuesday and Wednesday data should bring further confirmation that UK inflation is cooling and the job market remains weak increasing the room for the BOE to cut rates in the short term. Eurozone data on Thursday should indicate that confidence levels among the bloc’s consumers has risen back to the highest levels since October 2024. Thursday will also see the release of Irish inflation data for January with hopes for some deceleration from the 2.8% YoY pace of growth seen in the prior month. On Friday, data from the Eurozone should indicate industrial activity has turned higher for the first time in 3 months.

Across the Atlantic, data should indicate that the US economy closed out the final quarter in rude health with a GDP rate of 2.8%. This growth data combined with the delayed release of the Fed’s favoured inflation measure for December and FOMC minutes from earlier in the week should provide greater colour on the path for interest rates going forward. Finally, Friday could also see the Supreme Court rule on the legality of the IEEPA tariffs. Any limits applied on how IEEPA is used could see tariffs on consumer goods fall from c.15% to 12%.

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland