The Weekly Compass 02/06/26

John Mullane

John Mullane

02.06.2026

The Weekly Compass: 2/6/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead : US Job numbers and developments in the middle east the key focus in the week ahead.

The Week That Was

Global equities moved higher last week on positive developments in the Middle East, supportive corporate earnings and softer than expected inflation data. The S&P 500 climbed 1.4%, with the standout sectors being Consumer Discretionary and IT, with shares in Dell climbing 33% on Friday alone on strong AI server demand.

European equities edged up by a marginal 0.3% on the back of easing oil prices, which fell by 11% to $92 a barrel and dragged global commodities down 3.0% in euro terms on the week. The resultant easing of inflation expectations saw global bond markets move modestly higher on the week, with the US 10-year falling back below the key 4.5% level over the course of the week.

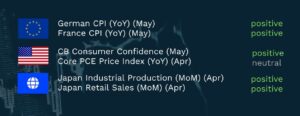

Summary Economic Releases

The Week Ahead

Asian equities traded sideways overnight, reflecting a degree of investor profit-taking alongside continued uncertainty surrounding the Middle East outlook. Brent crude retained most of the previous session’s gains, holding around $94 per barrel despite the Trump administration indicating that negotiations with Iran were progressing at a “rapid” pace. In corporate developments, it emerged that Anthropic has submitted an IPO filing, positioning the Claude AI developer as a likely landmark $1trn listing this year and further underscoring strong investor appetite for leading AI platforms. Meanwhile, Alphabet signalled an intention to raise $80bn to fund its expanding AI investments, with Berkshire Hathaway to be a key investor in the same.

From a corporate perspective, earnings releases remain light with the first quarter reporting season largely complete, leaving markets more driven by macro developments. Attention will stay firmly on the evolving US and Iran dynamic, where the potential signing of a memorandum of understanding this week to reopen the Strait of Hormuz could materially ease concerns around global energy supply and, by extension, inflationary pressures. Within the limited earnings calendar, Broadcom will be a key focus as investors look for further confirmation of the resilience of AI-related infrastructure spending. Elsewhere, the c. $13bn flotation of Honeywell-backed quantum computing company Quantinuum on Thursday will serve as an important gauge of investor appetite for emerging technologies. The week will also see a number of major tech conferences which could deliver market moving announcements from the likes of Microsoft.

From an economic perspective, US employment will be the key focal point in the week ahead, with JOLTS data due today likely to confirm a further increase in job openings in April. The release of May non-farm payrolls on Friday, where a gain of around 93k is expected, should help reinforce confidence in the recovery of the labour market and is likely to be sufficient to keep the unemployment rate broadly stable. In Europe, attention will turn to euro area inflation data also due today, with both core (2.4%) and headline (3.2%) readings expected to strengthen the case for an ECB rate hike later this month. In Asia, a continued uptick in Japanese wage growth, due on Friday, would further support the argument for additional monetary tightening by the Bank of Japan in the months ahead.

Opportunities this week:

- FedEx Express (Neutral, PT $320, 5% downside) – Post FedEx Freight spin valuation and PT/rating revision

- DCC (Overweight, PT 6960p, 17% upside) – Takeover watch and FY26 recap

- Infineon Technologies (Overweight, PT €90.50, +13% upside) – Increased PT given sector growth and expanded Nvidia partnership.

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.