The Weekly Compass 13/07/26

John Mullane

John Mullane

13.07.2026

The Weekly Compass: 13/07/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead : US Bank earnings the key focus in the week ahead

The Week That Was

Global equities closed the week broadly flat as renewed tensions between the US-Iran dampened investor enthusiasm ahead of earnings season. The S&P 500 climbed 1.3% buoyed by a strong rally in Technology with the IPO of South Korean memory chip producer, SK Hynix +13% and Communication Services with Meta climbing 15% as it rolled out a new AI model focused on image creation.

European equities fell by 1.8%, with defensive sectors such as Telecom’s outperforming led by Vodafone +11% as French telecoms mogul, Xavier Niel became its top shareholder. Global Commodities climbed 3.2% in euro terms with Brent Oil back at $76 a barrel as fresh attacks in the Strait of Hormuz resulted in an ending of the US-Iran ceasefire. Global Bonds were largely flat on the week whilst EUR/USD held steady at 1.14.

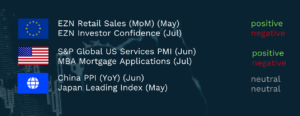

Summary Economic Releases

The Week Ahead

Asian markets trended lower this morning as the US conducted fresh strikes on Iran. This escalation in tensions also resulted in traffic through the Strait of Hormuz grinding to a halt and Brent spiking to $79.4 a barrel. The Japanese Finance Minister floated the idea of encouraging pension funds, to increase investment in domestic financial assets overnight, that provided some support for the Yen, which is trading close to its lowest level in decades. On the corporate side, TSMC posted 36% quarterly sales growth showing that AI hardware demand is still intact

The commencement of corporate earnings season should dominate market price action in the week ahead. US Banking bellwethers such as JP Morgan, Goldman Sachs and Morgan Stanley are all due to report. Overall, the sector is set to post earnings growth in the low double-digits with capital markets activities expected to be buoyed by increased volatility that kept trading at elevated levels and a step-up in corporate IPO activity positive on the Investment Banking side. Overall US earnings growth is forecast to climb by 23.6% for the quarter with Energy, Materials and Technology seeing the largest earnings revisions. Closer to home, earnings revisions have been trending higher in Europe with the Banking and Industrial’s sectors both having the potential to surprise positively. Stocks in focus include, Grafton provides a brief trading statement (covered below), Rio Tinto and TotalEnergies provide production and potentially guidance updates, where we expect Total to show strong trading profitability, whilst DCC’s AGM on Thursday will also be in focus given the looming Put-Up-Or-Shut Up deadline for the KKR and Energy Capital Partners’ offer.

From an economic perspective, on Tuesday, US core CPI is expected to hold steady at 2.8% for June despite a spike in leisure related activities due to the World Cup and the price of electronic goods due to the memory chip shortage. This data could ease pressure on the US Fed to hike however the ongoing skirmish between the US-Iran will also be playing on Kevin Warsh’s mind when he delivers his semi-annual testimony to congress. Thursday should bring confirmation that UK GDP edged up for the month of May whilst on Friday, investors will be looking for more details on Andy Burnhams policy priorities when he is set to formally become labour leader. Friday should also point to improving consumer sentiment in the US with the release of July University of Michigan data.

Opportunities this week:

- Smurfit Westrock (Overweight, PT $55.60, c.26% upside) – Newsflow update, mill safety and reiterated thesis.

- Grafton (Overweight, PT £12.05, 37% upside) – H1 Sales and Trading statement update.

- Infineon Technologies (Overweight, PT €90.50 23% upside) – Q3 results preview.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.