The Weekly Compass 18/05/26

John Mullane

John Mullane

18.05.2026

The Weekly Compass: 18/5/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead : Nvidia earnings the marquee event

The Week That Was

Global equities were mixed over the week as resilient corporate earnings and supportive economic data underpinned risk appetite. The S&P 500 was broadly flat on the week, with semis the standout performer, buoyed by the IPO of AI player Cerebras, which climbed 50% above its offer price. European equities ended the week 0.7% lower, with Energy the standout sector, as the ongoing stalemate between the US and Iran saw Brent climb almost 8% to $109 a barrel and contributed to EUR/USD retracing to 1.16. Global bond markets declined by close to 2% as concerns over a persistent inflation shock continued to drive yields higher, particularly at the long end of the curve.

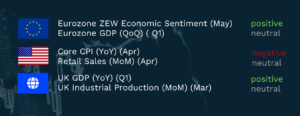

Summary Economic Releases

The Week Ahead

Asian equities traded lower this morning as rising borrowing costs across the G7, largely linked to ongoing tensions in the Middle East, continue to weigh on risk sentiment. Oil prices extended their gains, with Brent crude reaching $111 per barrel amid heightened geopolitical uncertainty. President Trump warned that Tehran is ‘running out of time’ to reach a peace agreement, though progress towards a resolution remains limited. Meanwhile, the recent summit between President Xi and Trump appears to have helped stabilise US-China relations, with announcements over the weekend suggesting tariffs would be reduced on certain goods. In addition, China committed to purchasing more than $17bn in agricultural commodities through 2028, providing some support to the broader trade outlook.

Earnings season is largely in the rear view mirror, but the results and guidance from the world’s largest company, Nvidia, will have a key bearing on the direction of markets in the week ahead. Investors will likely need to see a solid beat and raise on earnings, along with confidence in the sustainability of the current AI cycle. Elsewhere in the US, results from Walmart and Target will provide insights into how rising gasoline prices are impacting consumer spending. In Europe, Ryanair numbers this morning were solid for FY2026, but higher costs point to some margin pressure in 2027, though less so than peers. DCC will likely report stable energy results, but the focus will be on the takeover offer and management’s response. Investors will also pay close attention to results from Richemont to gauge whether rebounding luxury watch demand can offset the negative impact of rising prices.

From an economic perspective, Wednesday’s FOMC minutes are likely to be a key market-moving event as investors fret that elevated inflation could force the Fed to raise interest rates later this year. Data on Thursday is likely to indicate that industrial activity continued to expand in the US over May, but contracted in the Eurozone to its lowest level since November 2024. Consumer confidence is also expected to post its lowest reading since 2022 in the Eurozone, reflecting the impact of the ongoing conflict in the Middle East. From a geopolitical perspective, the UK political situation will continue to garner attention, given recent turmoil has seen its 30-year borrowing costs climb to the highest level this century, whilst investors will continue to watch for signs of progress in the Middle East.

Opportunities this week:

- Ryanair (Overweight, PT €30.50, c. 38% upside) – Post-FY26 results commentary

- Cairn Homes (Overweight, €2.83, +21% upside) – Read-across from Glenveagh Properties’ trading update

- Glanbia (Overweight, €22.90, +12.4% upside) – Updated PT after solid trading performance

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.