The Weekly Compass 13/04/26

John Mullane

John Mullane

13.04.2026

The Weekly Compass: 13/4/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: Q1 Earnings season and developments in Iran the key focus in week ahead

The Week That Was

Global equity markets staged a strong rally last week, with Emerging Markets particularly strong on the back of a ceasefire between the US and Iran. The S&P 500 climbed 3.6%, led higher by Consumer Discretionary and Communication Services, and now sits just 2% below its YTD highs. European equities moved 3.2% higher, with the banking sector leading the charge, whilst the euro also strengthened back to the 1.17 level relative to the USD. Oil prices declined c. 13% on the week, pushing commodities down close to 4.0%. Global bonds moved marginally lower, partly on a slightly hawkish tilt from Fed speakers.

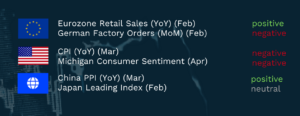

Summary Economic Releases

The Week Ahead

Asian markets moved marginally lower this morning following the failure by the US and Iran to come to an enduring agreement to end the conflict after talks in Pakistan at the weekend. The decision by the US to block the Strait of Hormuz whilst negotiations continue has resulted in Brent climbing back to $101 a barrel, however futures markets still see a return to the mid-$80s by Q4 of this year. The weekend also saw Viktor Orban’s 16-year reign as Hungarian PM come to an end. The opposition Tisza party is on course for a landslide majority and will be focused on rebuilding relations with European allies, along with rooting out Russian influence across its government.

Whilst negotiations between the US and Iran will continue to be a key focus, the commencement of US earnings will also garner plenty of attention. US banking giants Goldman Sachs, JPMorgan and Morgan Stanley are all due to report, with capital markets activity expected to be particularly strong, whilst a pick-up in commercial lending should also be evident. Outlook statements will be a key driver of market sentiment in the quarter, where earnings are expected to rise by 12.6%, a sixth straight quarter of double-digit growth. This growth will again be led by Communication Services and Technology, with Nvidia alone expected to account for 32% of the index’s quarterly earnings growth. Other names of interest that will report include ASML, TSMC, Tesco and LVMH, with the luxury goods player reporting Q1 results after the European close today.

From an economic perspective, on Tuesday some pass-through effects of the Iranian conflict are expected to be visible in US March Producer Price Inflation data, where the headline rate is expected to climb to 4.6% YoY. Wednesday’s Beige Book release will be the first forward-looking read of business conditions in Fed regions since the US-Iran war started. Thursday is likely to showcase that Chinese GDP growth accelerated in Q1, buoyed by a surge in production activity in the first two months of the quarter. Finally, on Friday, Eurozone trade data will likely indicate that US tariffs continue to weigh on export growth in February.

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland