The Weekly Compass 09/03/26

John Mullane

John Mullane

09.03.2026

The Weekly Compass: 09/3/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: Developments in Iran the key focus in the week ahead

The week that was

Global equity markets trended lower last week as elevated tensions in the Middle East, concerns about the health of private credit and underwhelming macro data weighed on sentiment. The weaker than expected US jobs data for February contributed to a 2.2% fall in the S&P 500 which posted its worst week since mid‑October. European equities closed down 5.6% on the week, erasing most of their year‑to‑date gains, with all sectors in the red except energy. The euro also weakened to €1.16 against the dollar, partly due to the Eurozone’s heavy reliance on imported oil and gas unlike the US. Global bonds were broadly flat on the week in euro terms but global commodities (+10.2%) were sharply higher on the back of a strong rally in oil prices.

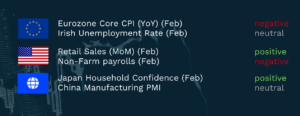

Summary economic releases

The week ahead

Markets in Asia have trended lower this morning on the back of escalating tensions in Iran and thus largely looked through better macro data. Chinese inflation accelerated to its fastest pace in three years, buoyed by robust Lunar New Year demand, while Japanese wages rose for the first time in almost 12 months. Iran’s election of the late Ayatollah Khamenei’s son as its new supreme leader, combined with Middle East oil exporters reducing output, sent Brent Crude briefly to $119 a barrel. Expectations that the G7 and the IEA will announce the release of significant petroleum reserves later today have seen Brent prices moderate to $107.

Developments in Iran will continue to be the key driver of market sentiment in the week ahead. The current environment is clearly unsettling for investors; however, the market impact of geopolitical tensions is typically short‑lived, with US equities for instance normally higher one month after the commencement of similar historic hostilities. This conflict looks no different, with de‑escalation likely in the coming weeks, which is reflected in oil price futures that see a retracement in Brent Crude below $75 a barrel by Q3 2026. The Trump administration will be under pressure to end the conflict as it is unpopular among the American public and any sustained rise in energy prices would negatively impact the Republicans’ chances in November’s mid‑terms. For Iran, any prolonged closure of the Strait of Hormuz would inflict further damage on an economy heavily reliant on oil exports. Nonetheless, tactical exposure to sectors such as oil and gas and defence should provide a hedge against short‑term volatility.

There will also be plenty of corporate earnings and macro data for investors to digest in the week ahead. On Wednesday, a slight softening in US core CPI for February should see the market look through a hotter January reading of the Fed’s preferred gauge, PCE later in the week. On Thursday, Irish inflation data for February is set to be released with some moderation from the 2.7% YoY rate expected for February. Also on Thursday, weekly jobless numbers will receive added attention given last week’s weak non‑farm release, however with three‑month average employment growth still running close to breakeven, the US labour market remains very much in a no‑hire no‑fire environment. On Friday, UK monthly GDP is set to have accelerated modestly for January as uncertainty around tariffs and domestic tax policy eased, while Michigan data is expected to indicate a moderate step down in US consumer sentiment for March. Earnings season is largely in the rear‑view mirror; however, investors will pay close attention to results from tech giant Oracle, German automakers BMW and Volkswagen, along with Irish homebuilder Glenveagh.

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland