The Weekly Compass 23/2/26

John Mullane

John Mullane

23.02.2026

The Weekly Compass: 23/2/2026

Our CIO, John Mullane, shares the latest Market News and Views and gives insights for the week ahead: US tariff recalibration and Nvidia earnings in focus

The week that was

Global equity markets moved higher on the week, buoyed by a rebound in global tech and a decision by the US Supreme Court to strike down the use of IEEPA (International Emergency Economic Powers Act) tariffs. The S&P 500 climbed 1.1% supported by a rally in the Mag‑7 (+3.2%) along with more value‑orientated names, with strong earnings from bellwethers such as John Deere (+9.9%).

European equities closed up 2.2%, led by a strong rebound in the banking sector, with Societe Générale +10.6% and Bank of Ireland +6.8% among the standout performers. Global bonds moved up by a modest +0.5% whilst global commodities (+2.9%) continued their robust start to the year, with oil particularly strong on rising tensions between the US and Iran.

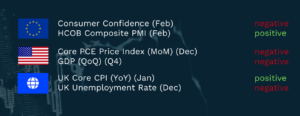

Summary of economic releases

The week ahead

Markets in mainland China and Japan are closed today. Nonetheless, Asian benchmarks started the week on the front foot with tech stocks particularly strong as investors continue to digest the implications of the changing tariff landscape. In aggregate, Asian economies will see tariff rates fall from 20% to 17% following President Trump’s decision over the weekend to implement a 15% global tariff.

The EU may delay ratification; however, the necessity of US security guarantees to ensure a lasting peace in Ukraine means the trade deal will likely remain largely unchanged. This US policy uncertainty has resulted in a modest decline in the Dollar versus the Euro and a strengthening of safe havens such as gold this morning.

Corporate earnings, and particularly the performance of Nvidia, will be a key focus in the week ahead. The world’s largest company is broadly flat year to date and its valuation has derated in recent months, meaning a strong beat and raise could act as a catalyst for the stock and the sector more broadly.

Elsewhere in the US, Home Depot and Flutter will report, with the latter expected to deliver strong earnings. All ears will be on what the company says about prediction markets in terms of their impact to date, as well as Flutter’s plans for product launches and support spending. Overall, 74% of S&P 500 companies have now reported, with the earnings beat rate running at over 70%.

In Europe, earnings season is past the midway point and whilst regional share price performance has been strong, in aggregate earnings revisions have been negative. Key names due to report from an Irish perspective are Diageo, Uniphar and Glanbia. For the latter, the market will be keen to see margin stability and growth within the group’s Performance Nutrition segment, commentary on whey input costs and potential growth drivers from the rollout of GLP‑1 medications.

It will be a busy week on the macro front with plenty of market‑moving data. The German IFO reading for February is expected to turn higher for the first time in four months and with consumer confidence also expected to improve on Wednesday, this could point to a modest acceleration in GDP for the quarter. Across the Atlantic, whilst last week’s miss on GDP was primarily due to the government shutdown, macro data will nonetheless face increased scrutiny.

On Tuesday, consumer confidence is expected to bounce back in February on falling inflation expectations, whilst ADP employment data will also garner attention. Tuesday will also see Trump’s State of the Union address, where the market is likely to get more colour on the recalibration of US tariffs and potential measures to tackle the affordability crisis. On Friday, inflation in Germany and Spain is expected to trend lower whilst a step‑up is expected in France; underlying dynamics across the Eurozone remain muted. In the US, producer price rises will be watched closely as any resurgence could lead to delays in rate cuts.

This is an extract from the Weekly Markets Report by Cantor Fitzgerald Ireland. For more detail on individual securities, or to discuss how we can support your investment needs, please get in touch.

Written by John Mullane, CIO, Cantor Fitzgerald Ireland