Investing: The Basics

John Mullane

John Mullane

25.02.2026

Investing in Ireland: The Basics

Irish households currently hold more than €170bn in bank deposits, yet with rates on savings low and inflation eroding the real value of each euro over time, leaving money idle can mean missing out on meaningful growth opportunities. Whilst investing in higher-returning assets can seem daunting or complex at first, understanding the basics and seeking out the right level of guidance can help ensure your money works harder in helping you achieve your long-term goals.

Step 1: What You Need to Begin

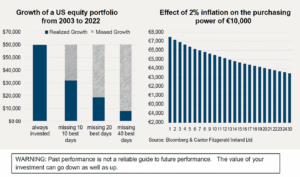

Before investing, the most important step is to get clarity on your personal goals. Some people invest for retirement; others want to achieve specific financial objectives such as paying for their children’s education, whilst many simply want to ensure their savings outpace inflation.

Step 2: What You Can Invest in

There’s a broad range of instruments available across financial markets, which can typically be broken down into three major asset classes.

- Shares (Equities): Investing in shares allows you to own part of a company, thus enabling you to benefit from capital growth and any dividends it may pay. While equities historically offer attractive long-term returns, they can be volatile in the short term.

- Bonds (Fixed Income): Investing in bonds means you are effectively lending to a government or corporate entity, in return for which you usually receive regular coupon (interest) payments along with your capital back at maturity. As an asset class, bonds generally offer inferior returns relative to equities but also have lower volatility.

- Alternatives: These represent a broad-church of assets that have varying risk and return profiles. These range from gold, which can act as a hedge against inflation and geopolitical volatility, to private equity, which offers access to high-growth, early-stage companies but comes with higher risk.

Most of these assets can be bought as standalone investments or as part of diversified investment vehicles such as exchange-traded funds (ETFs). Choosing the right mix of these assets is crucial in helping you achieve your investment objectives. Allocating to these assets through a pensions structure is one of the most effective and tax-efficient ways to build wealth in Ireland.

Step 3: Choosing Your Service Level

The service level that suits you depends on your experience level and how actively involved you want to be in decision-making with three main options:

DIY or execution-only option: This option is highly accessible either through a wealth manager or online platform. You can access a wide variety of instruments ranging from direct shares and bonds to passive and active ETF’s. Picking the right instrument can be difficult and as each investment decision rests with you and failure to keep abreast of constantly evolving market dynamics can prove costly. As a result, its usually best suited to highly experienced investors who have a good knowledge of financial markets and have the time to monitor them closely.

Advisory option: Many investors will enlist the services of their local financial advisor to help them select suitable investments. In most instances, an advisor will suggest investing in a collection of pooled investment fund or securities that most closely aligns with your financial goals, risk tolerance and time horizon. You will get benefit of expert advice but will remain ultimately responsible for all investment decisions, fees can vary significantly, and it may not be the most tax efficient solution for your needs. As a result, it’s important to consider how much time you can dedicate to investment decision making along with carefully researching and comparing advisors before committing.

Discretionary Investment Service: This is often the preferred option for those seeking a more tailored and professionally managed solution. Through this wealth management service, your portfolio will be actively managed on your behalf by a professional fund manager in accordance with your investment objectives and risk profile. These assets are held in your own dedicated account, which provides you with greater transparency and thus comfort on how your money is being managed relative to an off the shelf pooled fund. This approach is typically quite tax efficient and comes with a premium service, which may also result in a higher headline cost.

Why Advice Matters

Even small missteps in areas such as portfolio construction, taxation, fees or timing can negatively impact long-term returns. As a result, seeking advice from a qualified and experienced financial advisor can make a meaningful difference in helping to ensure your hard-earned income works as hard as you do.

Get in touch today to discuss how we can support your investment needs.

By John Mullane Chief Investment Officer, Cantor Fitzgerald Ireland